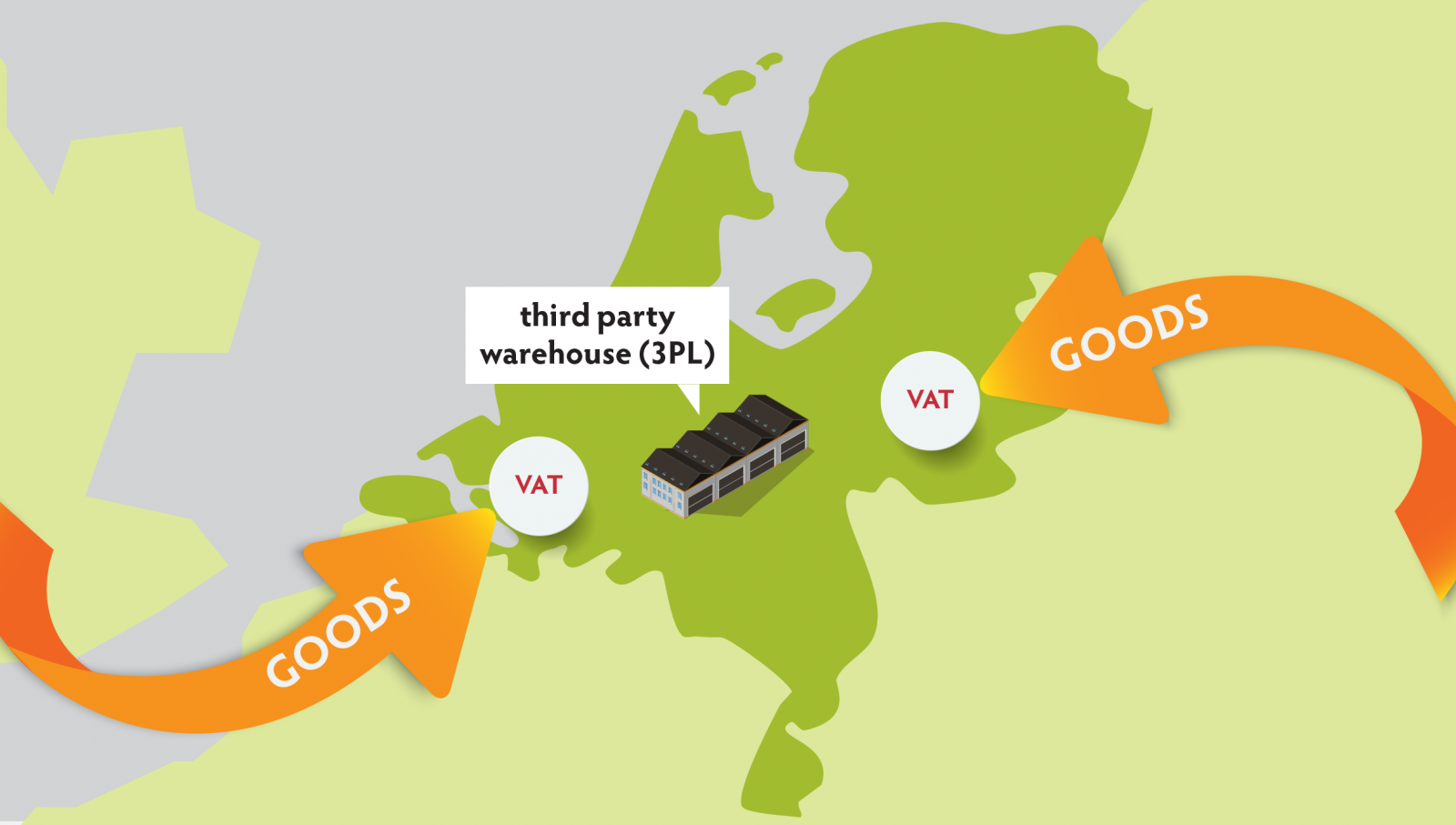

When the amounts and the number of transactions are limited, the company may choose to pay the VAT at the border and reclaim it via a tax return on a quarterly base.

As a rule, there is some time (a few months) between the moment when the VAT is paid at the border and the return receipt via the tax return.

When delivering the products to other companies (B2B, both inside and outside the EU), the company makes use of deferral of the VAT to the customer.